The bubbles in CNN

8 January 2015

No, this is not about a TV network. We're going to take you on a tour of what we call the Chung Nam Network (CNN), involving numerous HK-listed companies which do very little but trade with each other and in each other's stocks, sucking in cash from the markets and creating occasional bubbles. In many cases, the cross-shareholdings are kept below the 10% level at which the Stock Exchange would treat them as connected parties, and often below the 5% level at which disclosures of interests must be filed by law, so not all of it is visible, but we can sometimes spot sub-5% shareholdings in financial statements.

We'll tell you about 3 stock bubbles amounting to HK$20.0bn (US$2.58bn) - but the key message is to avoid any stock in the CNN. If they were the last stocks in the universe, we wouldn't buy them. We'll also mention a fourth bubble outside the network.

Hao Tian

We'll start with CNN member Hao Tian Development Group Ltd (HTD, 0474) for an example of what we regard as one of the most blatantly false and misleading statements of 2014.

On 4-Jul-2014, HTD announced the grant of a 2-year call option over 240m shares (3.00%) of Imperial Pacific International Holdings Ltd (Imperial, 1076) to one Jiang Jianhui (姜建輝) for HK$5m, or about $0.02083 per option share, at an exercise price of $0.55 per share, a discount of 22.5% to the market price of $0.71. Yes, you read that right. The options had an intrinsic value of $0.16 per share plus the time value of the option, but he/she was paying only $0.02083. At the time, HTD owned 276m Imperial shares, for which it had paid $0.166 per share. We have no idea who Mr/Ms Jiang is.

So what was the reason for granting the option? HTD said:

"The Call Option Deed provides the Group with the right to sell the Option Shares at the Exercise Price, which is higher than the average per share cost for acquisition of the Option Shares, allowing the Group to hedge against a possible fall in the value of the Option Shares"

Which is completely false, of course. They had sold a call option, not bought a put option. What it should have said is:

"The Call Option Deed provides the Optionholder with the right to buy the Option Shares at the Exercise Price, which he/she will probably do by expiry if the market price is higher than the exercise price, allowing the Group to give up the upside while remaining exposed to a possible fall in the value of the Option Shares"

The Directors (their names are here) considered this to be on "normal commercial terms" and fair and reasonable". Now, because of fair value accounting, the interim report for the 6 months to 30-Sep-2014 had to tell you just how unreasonable this was. Note 12(iii) on page 44 shows that based on the directors' own assumptions, when the option was granted, it was worth HK$73.763m, resulting in an instant loss of $68.763m. By 30-Sep-2014, the market price of Imperial had risen to $1.64, and the option was worth HK$270.713m, resulting in a further loss of HK$196.95m, or a total book loss of $265.713m.

In our view, no reasonable board could say that selling something worth $73.8m for $5m was "fair and reasonable". It is what lawyers call Wednesbury Unreasonable and, if HK allowed class actions (which it doesn't) then shareholders would have a good chance of successfully suing the directors for breach of fiduciary duty.

Imperial is not part of the CNN by the way, but it is a bubble surrounding a Macau junket operation and a casino project in Saipan, Northern Mariana Islands. Click here for our side piece on that.

Heritage

On 28-Jul-2014, HTD bought 575.25m shares of another CNN member, Heritage International Holdings Ltd (Heritage, 0412) off-market at $0.94, and the next day it bought 240m shares off-market at $1.00, for a total of 815.25m shares (28.87%) a total cost or "consideration" of $780.7m. Some of these probably came from HEC Capital Ltd, which disposed of 100m shares at $1.00 on 28-Jul-2014, and Willie International Holdings Ltd (Willie, 0273) which disposed of 25m shares at $1.00, both cutting below 5%. Our guess is that the other shares probably came from other companies in the CNN which each held less than 5%.

Undisclosed Very Substantial Acquisition

The 5-day average price of HTD up to 28-Jul-2014 was $0.1538, so its market capitalisation was $610.9m. Divide that into the consideration and you get a "consideration ratio" of 128%, which makes it a Very Substantial Acquisition under Rule 14.08 of the Listing Rules, but HTD did not make any announcement about this or obtain shareholders' approval.

Since then, Heritage has done a 1:2 bonus issue, so HTD now owns 1,222.875m shares. The HTD interim report disagrees though. It says in note 17 that HTD bought 740m shares, or 1110m shares (26.20%) after the bonus issue. The gap is not explained. Meanwhile, the Heritage interim report at 30-Sep-2014 says that HTD owns the full 28.87%.

The HTD report also says that HTD "has irrevocably undertaken to Heritage that the Group shall not participate or otherwise exercise any influence" over Heritage, which handily allows HTD to account for this as an investment at market value rather than as an associate. There's been no announcement from Heritage about HTD becoming its largest shareholder or the undertaking.

By 30-Sep-2014, Heritage shares, after the bonus issue, had shot up to $2.10, valuing HTD's stake at $2568m, which explains most of the huge "fair value gain on investments held for trading" of $1596m booked in the interim results. At yesterday's closing price of $1.52, HTD's stake is worth HK$1859m, while HTD had a market value of HK$946m. Don't get too excited though, because Heritage is in a bubble as we explain later in this article.

Freeman Corp Ltd

On 6-Oct-2014, Freeman Corp Ltd (FC, Cayman) bought 100m shares (2.36%) of Heritage at $2.00 off-market, increasing from 4.97% to 7.33%. FC is majority-owned by Freeman Financial Corp Ltd (Freeman, 0279). FC is one of two large unlisted companies at the core of the network, what we'll call "hubs", the other being HEC Capital Ltd (HECC, Cayman). The listed companies pump money into the unlisted hubs, which own brokerages and trade the stocks of the members, either for the hub's own account or as agents of the companies.

HECC is the older hub and owns HEC Securities Ltd (formerly Chung Nam Securities Ltd, hence the network name), while FC owns Freeman Securities Ltd. The whole thing is a moving target, but as of 26-Nov-2014, according to page 9 of a Freeman circular, FC was owned by the network as follows:

| Shareholder | Stock code | Stake % |

|---|---|---|

| Freeman | 0279 | 60.52 |

| Willie | 0273 | 23.86 |

| Forefront Group Ltd (Forefront) | 0885 | 7.16 |

| Dragonite International Ltd (Dragonite) | 0329 | 4.37 |

| China Jinhai International Group Ltd (China Jinhai) | 0139 | 2.41 |

| National Investments Fund Ltd (NIF) | 1227 | 1.67 |

| Total | 100.00 |

Heritage and Rising Development: one bubble inside another

Heritage had a Webb-site Total Return of 368.37% in 2014, so you might think there was something good going on there, but in our view, it is one tightly-held bubble around another. A double bubble! In the interim report at 30-Sep-2014, it had net tangible assets (NTA) of HK$750.5m, or $0.177 per share, compared with a share price on that date of $2.10. Of the NTA, $340.8m was unlisted equities, including at least $288m injected into HECC on 12-Jun-2014, and $461.5m of unnamed listed equity investments at market value.

Note 25 of the Heritage annual report at 31-Mar-2014 reveals that Heritage then owned 4.58% of Rising Development Holdings Ltd (Rising Dev, 1004), below the 5% disclosure threshold. That's about 68.07m shares, then worth about HK$293m at $4.30 per share. By 30-Sep-2014, Rising Dev had risen to $6.90, so if Heritage still held it, the gain was about $177m and the stock was worth about $470m. That roughly fits, because Heritage booked unrealised gains on investments of $167.95m for the period.

Rising Dev's stock split 4:1 on 19-Dec-2014, and closed at $1.24 yesterday, so it is down by 28% since 30-Sep-2014. That knocks about $132m off the value of Heritage's stake already. We'll add back deferred profits tax because this is a "trading" position, so the Heritage NTA is down by about $110m, reducing it to about $640m or $0.151 per share.

Yesterday (7-Jan-2014) Heritage closed at $1.52. It plans to split 4:1 on 23-Jan-2015. The market capitalisation is HK$6439m, but that is about 10.1 times its pro forma NTA, and as we have shown, the NTA depends mainly on just two assets: shares in HECC and Rising Dev, which is in a bubble itself.

Rising Dev has generated a certain amount of excitement by buying or planning to buy various solar power plants in China, but you just need to focus on one key page in the New Year's Eve deal circular: that's the pro forma adjusted NTA on page 213 of the PDF, which shows $430.1m, or $0.0616 per share. The rest is just hot air. After that deal, there will be 6988m shares in issue. At yesterday's closing price of $1.24, that values Rising Dev at about HK$8665m, or about 20.1 times NTA.

So like Russian dolls, you've got one bubble inside another. It's really quite clever. If you valued the Rising Dev shares that Heritage owns based on the underlying NTA of $0.0616 per share, then the stake would be worth about $17m, making the Heritage price look even more ridiculous.

Following a complaint from Webb-site, the SFC recently warned the market that at 10-Oct-2014, a small group of 20 shareholders held 93.71% of Rising Dev. In other words, it has probably been cornered. Rising Dev had a Webb-site Total Return of 537.97% in 2014, and you can see the comparison with Heritage in this chart.

Network hub FC owns 6.41% of Rising Dev at 19-Dec-2014.

Rising Dev started life as a fur trader, listing on 9-Oct-1997. On 22-Jul-2007 Lai Leong (Mr Lai) agreed to buy 71.63% of the company from its founders for H$K400.2m, triggering a general offer on completion.

Chairman Mr Lai now owns 23.74%, and one Cao Zhiying (Cao, 曹志鶯) apparently bought 16.15% (now 960m shares) off-market for $1560m (US$200m) on 29-Sep-2014. This was part of a sale of a 20.86% sale by Mr Lai. We have no idea who Mr/Ms Cao is. Another outsider is Huang Rulun (黃如論) who also calls himself "Wang Rulan" on his disclosure form, who increased from 4.49% to 7.79% of Heritage on 13-Dec-2014. Maybe it is this guy.

CST Mining

Another company at the periphery of the CNN that has bought into both the Heritage and Rising Dev bubbles is CST Mining Group Ltd (CST Mining, 0985), which owned below 5% of Heritage until 3-Nov-2014, when it bought 210m shares (4.96%) off-market at HK$2.00, a total of HK$420m, raising its stake to 9.81%. No vendor was visible.

Similarly, on 16-Dec-2014, CST Mining became a disclosed shareholder of Rising Dev, buying 50m shares (3.37%) at $5.33, raising its stake from 4.37% to 7.74%. After the stock split, it owns 460m shares.

CST Mining also held 23.8m shares in network hub HECC at 30-Sep-2014, or 2.38% of the issued shares.

Mission Capital

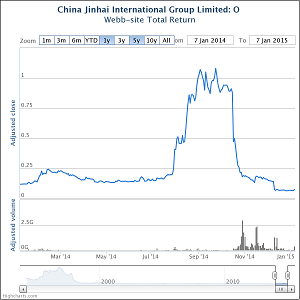

Another CNN member that holds or held both the Heritage and Rising Dev bubbles is Mission Capital Holdings Ltd (MC, 1141). Note 12 of its interim report at 30-Sep-2014 shows that it held 59.4m shares (4.00%) of Rising Dev, then worth HK$409.9m, and 190,037,500 shares (4.49%) of Heritage, then worth HK$399.1m. MC also held 457.34m shares (11.14%) of China Jinhai (then known as "ICube Technology Holdings Ltd") then worth $411.6m. It has since cut below 5% of China Jinhai, dumping during a price collapse on 21-24-Oct-2014.

Unmentioned in the report is that MC also holds 9.64% of Willie, having increased its holding from 4.99% on 3-Sep-2014, buying 35m shares off-market at $1.50. Those shares probably came from Unity Investments Holdings Ltd (Unity, 0913) which sold all its 55m shares off-market at the same price on the same day. Unity is a closed-end investment company in the CNN. After a bonus issue, MC held 90.75m Willie shares at 30-Sep-2014, then worth $127.0m. After an effective 15:1 split, MC now holds 1361.25m Willie shares, still 9.64%.

Mission also injected HK$228m into network hub HECC on 30-Jun-2014, increasing its holding to 41m shares (then 4.23%), with a book value of $246m at 30-Sep-2014.

Add that all up and you get at least $1594m of CNN investments in the balance sheet, and there are probably more.

Cordoba Homes

On 6-Jan-2015, MC agreed to subscribe 22m shares (5.46%) of Cordoba Homes Ltd (Cordoba, BVI) for HK$103.4m. The announcement doesn't say who owns Cordoba, but at the last disclosure on 18-Sep-2012, it was 100% owned by HECC. This will be reduced to 94.54% by the subscription. Watch out for more companies in the CNN to start investing in Cordoba, which is involved in residential and commercial properties in HK, artwork, paintings and money-lending. HECC owns 9.19% of MC, just avoiding the 10% threshold at which this would be a connected transaction.

The proposed investment comes 19 days after MC announced on 18-Dec-2014 a proposed 1:2 open offer of new shares at $0.10 to raise $209.66m, underwritten by HEC Securities Ltd, which is also owned by HECC.

Unity

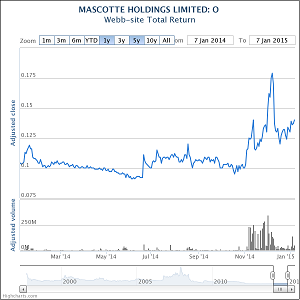

According to its interim report at 30-Jun-2014, Unity owned 4.97% of Heritage, just below the disclosure threshold. That was worth about $95m. According to a circular dated 12-Sep-2014 which gave further information on the 30-Jun-2014 positions, Unity held 4.91% of Forefront, 3.60% of Mission Capital (then Poly Capital Holdings Ltd), 0.32% of Rising Dev and 1.34% of Mascotte, which brings us on to:

Mascotte bubble

Another bubble in the CNN is Mascotte Holdings Ltd (Mascotte, 0136). At 31-Dec-2014, it had about 26.893bn shares outstanding, or more than 3 per person on the planet. There were also $700m of bonds outstanding which are convertible at $0.09 per share into another 7.778bn shares. The total then is 34.671bn shares worth HK$4854m at yesterday's closing price of $0.14.

The interim report at 30-Sep-2014 shows a net tangible deficit of $41.6m. Add back the convertible bond liability component of $52.2m and you've got $10.7m. On 29-Dec-2014, Mascotte granted 200m 10-year options to "certain employees", all of whom chose to exercise them the next day, at an exercise price of $0.134, raising $26.8m, and taking pro forma NTA to $37.5m, or about $0.00108 per share. So Mascotte is trading at about 129 times NTA.

At 30-Dec-2014, network hub FC owned 1564m shares (5.82%) of Mascotte, Andrew Liu owned 3344m shares (12.43%) and Nexus Emerging Opportunities Fund SPC (Nexus) owned 1000m shares (3.72%). Viola Mak Siu Hang and Nexus each owned $350m of convertible bonds.

© Webb-site.com, 2015

Organisations in this story

- Aceso Life Science Group Limited

- Arta TechFin Corporation Limited

- Central Wealth Group Holdings Limited

- China Ruyi Holdings Limited

- China Smarter Energy Group Holdings Limited

- CMBC Capital Holdings Limited

- CST Group Limited

- Freeman Corporation Limited (KY)

- Harbour Digital Asset Capital Limited

- HEC Capital Limited

- Imperial Pacific International Holdings Limited

- MASON GROUP HOLDINGS LIMITED

- National Investments Fund Limited

- OCI International Holdings Limited

- Rentian Technology Holdings Limited

- SHANDONG HI-SPEED HOLDINGS GROUP LIMITED

People in this story

Topics in this story

Sign up for our free newsletter

Recommend Webb-site to a friend

Copyright & disclaimer, Privacy policy